Contingent workforce program managers have consistently been required to deliver savings across their programs. In a program’s early days, the savings are based on percentage of spend when transitioning from a maverick approach to a more structured hiring methodology, such as either an internal or external MSP can be significant. However, as programs mature, such savings reduce and it becomes more challenging to demonstrate cost reductions year over year, especially when the cost of services — e.g., contingent workers’ wages — are, in fact, increasing.

But savings are still feasible. I recommend that program managers look at four key areas and ascertain what hard and soft cost savings are possible within each.

- Internal. As the buying entity, look into what could you do better.

- External (supply chain). What could entities such as the MSP and your staffing/other partners do better?

- Pay rate. What can be done over and above simply reducing pay rates?

- Statutory costs. Differentiate between the ongoing and the one-off legislative expenses.

Each of these four areas requires an in-depth brainstorm of all the things that could potentially provide either a hard or soft cost benefit to the organization.

Hard or Soft Savings?

Before we look at how to calculate savings and their impact on the organization, it’s necessary to understand the difference between hard and soft cost savings.

Hard. Hard savings are achieved on spend that is already committed to the ledger. This is committed spend which, when reduced, contributes to the bottom line of the organization.

For example, suppose a contingent worker is on a six-month assignment at a bill rate of £50 per hour. Halfway through the assignment, a revised bill rate of £48 per hour is negotiated for the next three months. This is a hard cost saving, as we are generating an improvement on the last three months of previously committed spend.

Soft. Soft savings can be considered as avoiding future spend that is not yet committed, such as negotiating preferential rates for future purchases or generating process efficiencies and converting them to a monetary value.

For example, say there is another contingent worker on a six-month assignment at a bill rate of £50 per hour. A six-month extension is then negotiated at a revised bill rate of £48 per hour. This is a soft cost saving, as we are generating an improvement on a new six-month assignment of previously uncommitted spend.

Both. It’s possible for savings to be a mix of hard and soft. For example, suppose that following a negotiation, the MSP fee is reduced from x% to y% (as a percentage of spend under management) on all workers with immediate effect. This can be considered a hard cost savings for any workers currently on site (committed spend) and a soft cost savings for any future hires (non-committed spend).

Identifying Savings Opportunities

Now let’s turn back to the four key areas from which programs can find opportunities to save. Brainstorm these items under the following headings:

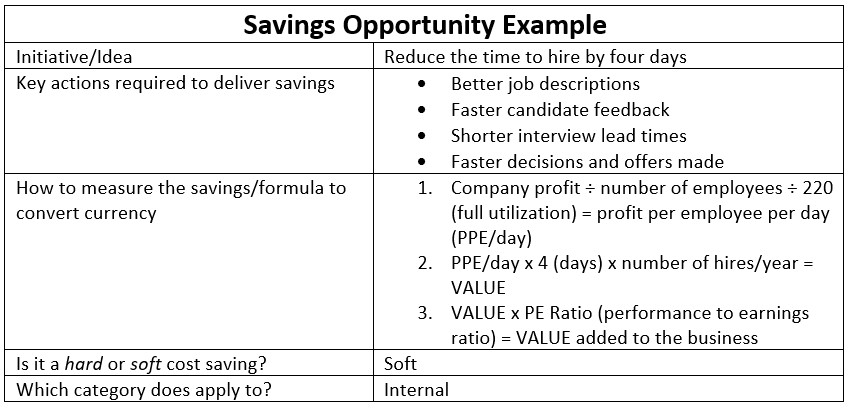

- Initiative/idea

- Key actions required to deliver savings

- How to measure the savings/formula to convert currency

- Is it a hard or soft cost saving?

- Which category does it apply to?

Item 3 is often the most challenging, especially when converting efficiency/activity improvements into a monetary value that impacts the organization.

Here’s an example of how to do this:

You are going to have to use a whole lot of assumptions when putting these together, but at least you will have a framework that, if challenged, can be amended.

By undertaking this exercise, you will be appealing to the executive suite who are most interested in profitability, shareholder value and market competitiveness. Their adoption of your program and the change necessary to be a success is therefore more likely.