Independent contractors are a growing contingent workforce population. The growth in talent-sourcing channels such as direct sourcing, statement-of-work solutions and on-demand/human cloud channels — along with the overall growth of gig economy engagements — all point to this fact. Recent SIA buyer research backs that up, showing usage of ICs could increase to 54% from 13% over the next 10 years.

This trend belies past trends that indicated a serious reluctance among contingent workforce program managers to engage independent contractors, with some buyers even creating program policies that prohibit their use.

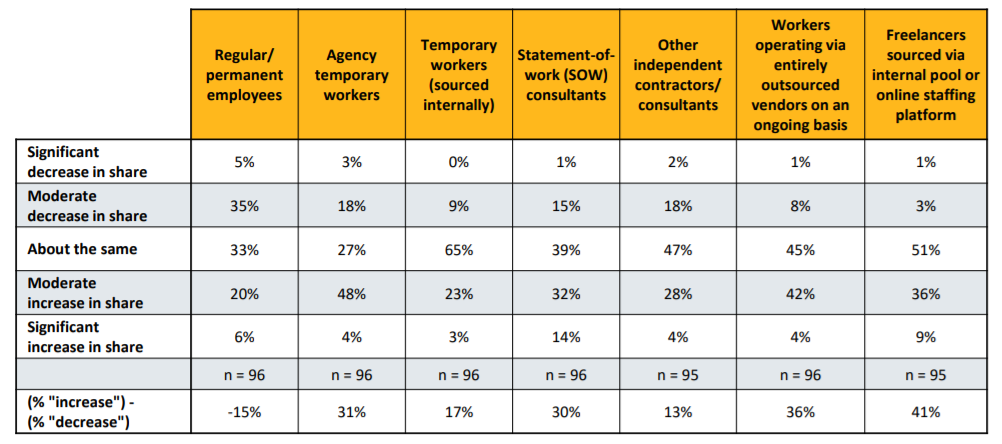

How employee types will change as a share of respondents’ total labor force over the next 10 years.

Source: Workforce Solutions Buyer Survey 2020

Still, CW managers are wont to proceed with caution.

Regulatory Ramifications

There are many potential consequences of improperly misclassifying a worker as an independent contractor. Some of the major consequences of misclassification are:

- Tax, interest and penalties. For unpaid employment taxes not withheld.

- Disqualification of otherwise qualified benefit plans. Failure to include eligible workers could cause 401(k) plans to lose status as qualified plans for IRS purposes. This would be a very bad outcome.

- Fair Labor Standards Act and other employment law liabilities. Failure to consider workers as your employees could lead to violation of multiple state and federal laws covering employees.

- State unemployment. A very significant source of classification conflict arises out of worker contact with state unemployment agencies. Misclassification is often detected by these agencies.

- Benefits eligibility. Workers improperly classified as ICs may be eligible for back benefits that they have been denied

- Immigration non-compliance. If workers are employees, they must have a valid I-9 form completed for them.

Laws and factors upon which worker classification depends:

- State ABC test/statutes

- Wage-and-hour laws

- Title VII of the Civil Rights Act/Americans with Disabilities Act/ Age Discrimination in Employment Act

- Workers’ compensation

- Unemployment Insurance

- Corporate benefit plans

- Federal agency regulations (Department of Labor, etc.)

IC Wariness

Contributing to program managers’ reluctance to use ICs is that federal, state and local governing authorities are implementing rules and legislation — California’s AB 5 and the UK’s IR 35 off payroll regulation, for example — to address some consequences of increased IC usage, such as lost tax revenue or perceived (real or not) business efforts to avoid marketplace wage and employment regulations. But in most cases, the use of IC talent can be a very attractive business model that allows stable, flexible, cost-effective, just-in-time access to required skill sets.

With all this increased usage and the emergence of government rules and legislation, it is imperative that CW program management professionals review, enhance and execute well-crafted risk mitigation and management strategies for IC engagements.

This can be tough with the fast pace at which the legal landscape is evolving with regard to IC classification status, leading to general confusion over the rules. There are numerous changes that continue to occur at both the federal and state government levels, such as California voters passing a proposition that allows platform drivers to remain independent contractors despite AB 5 and the US Department of Labor releasing its final rule last week on IC classification, which President-elect Biden is expected to pause upon his inauguration.

Managing Your IC Engagement Risk

Fundamentally, programs must track and understand all these more rapidly occurring federal and state IC rules changes — with the aid of trusted sources and subject-matter expert counsel.

Some of the basic steps that every business can take to improve the risk management and even the quality of its IC classification are:

1. Self-audit. The first step is knowing who within your program is an IC and why. Next, it is important to get a handle on how many ICs you have and whether they are properly classified or misclassified. Also examine how current ICs were engaged and whether they were engaged within or outside of your current classification program, if you have one. In other words, you are partly interested in whether your current system works, but you are also interested in determining whether the system is being utilized or disregarded.

2. Determine adequacy of classification system. Based on what you learned from the self-audit, decide if your current classification system is adequate and/or is properly enforced.

3. Modify your classification system. As needed, consider whether or not outsourcing of assessment of the process or parts of the classification process is a good idea.

4. Examine benefit plans. Amend your corporate benefit plan as necessary. Remember, Microsoft lost the $97 million Vizcaino case because its employee benefits plan did not exclude contract workers.

5. Consider IC compliance vendors. There are firms to which you can outsource investigation of IC status for your 1099 candidates. In a recent SIA buyer survey, 67% of respondents reported they are engaging IC compliance services/technology/payrolling services to execute their IC risk mitigation and management strategies.

It’s time to review and enhance your organization’s IC risk mitigation and management strategy. The independent contractor classification is being engaged more and more in the marketplace. As a result, expect more rules and regulations from governing authorities because of negative consequences that they believe, rightly or wrongly, need to be addressed.