Staffing Industry Analysts’ perspective on recent employment numbers can be helpful. The latest data from the US Bureau of Labor Statistics show notable growth in education and construction, but manufacturing, industrial and transport sectors are continuing their decline that started as the US dollar began strengthening in mid-2015. The mining sector has been hard hit by contractions in the oil and gas market, with jobs declining by 16.1% over the past year — the only area of the economy in which employment has actually contracted in that time.

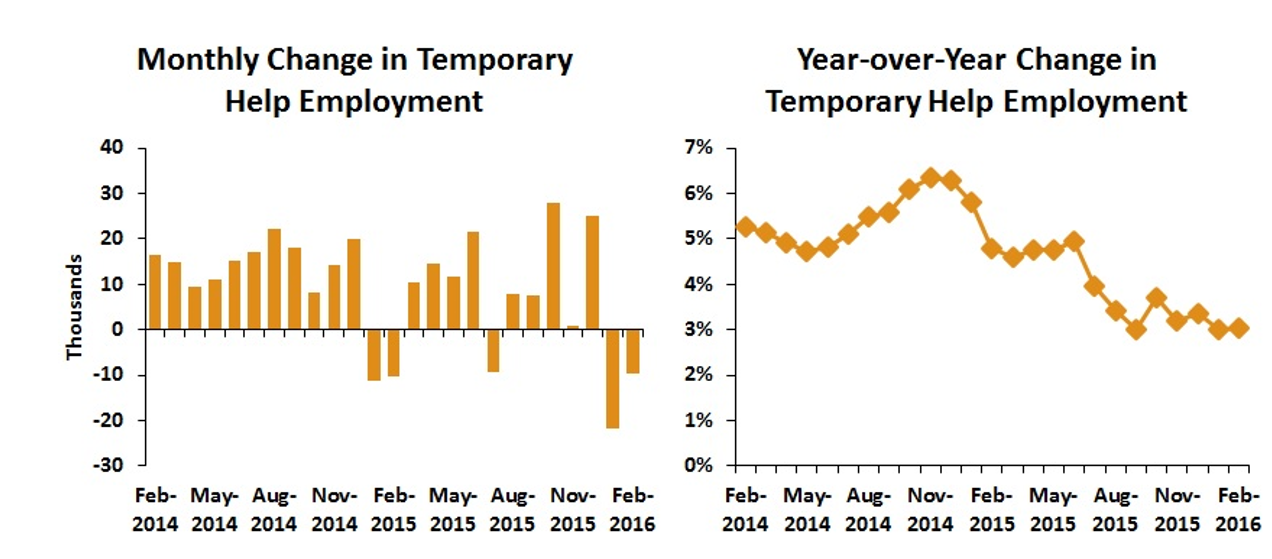

Will buyers be looking at more or less temporary help? Temporary jobs were down by 10,000 in February and have decreased 3.0% year over year. February was the second straight month of contraction for the industry. The year-over-year growth rate for temp help is now at about 3%, down from 6% rate posted in late-2014. However, last year also saw declines in temp jobs and the penetration rate before returning to growth in subsequent months. Could this be the BLS’s seasonal adjustment factors? Only time will tell; perhaps contingent work is being engaged through SOW or other channels more fully. These charts illustrate the trends for temporary help employment month over month and year over year:

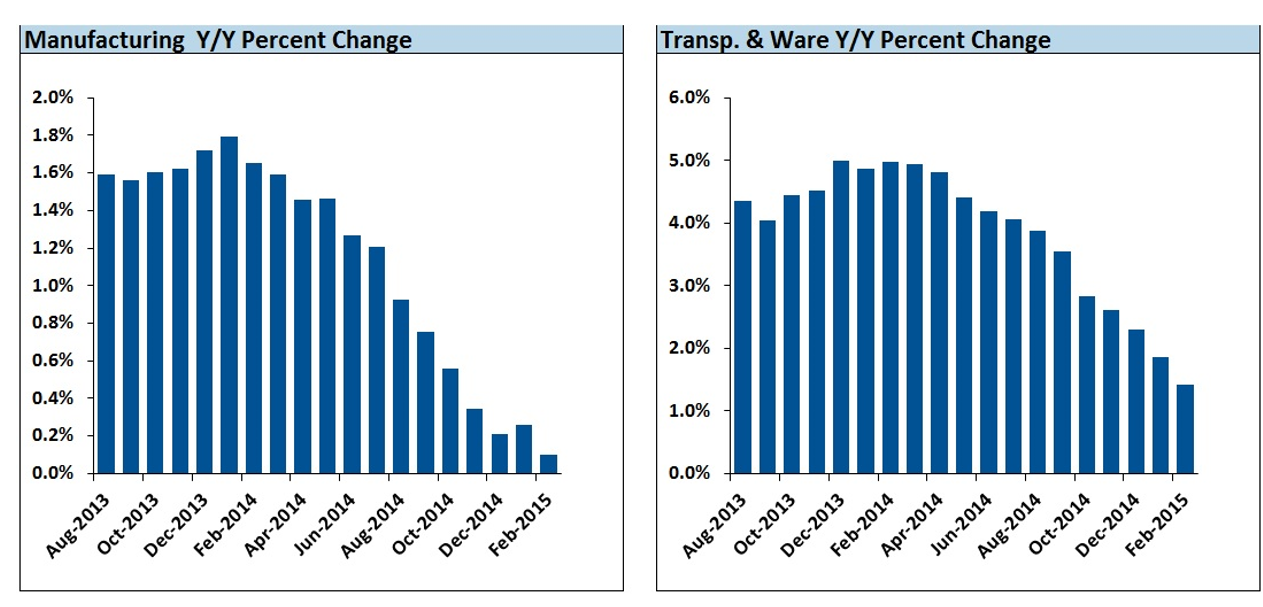

There is also visible deceleration in two of the biggest temporary help markets: manufacturing and transportation and warehousing.

Other temporary employment sectors contingent workforce managers may be interested in include healthcare, which was up 3.5%; professional services increased 3.2%; construction rose by 4.0%; and leisure/hospitality was up by 3.0%. Expect the demand-side economy to continue in these sectors and make sure your suppliers are actively recruiting and providing the talent you need based on where your companies’ interest lie. The unemployment rate continues to be low at 4.9%, and GDP increased at an annual rate of 1.0 percent in the fourth quarter of 2015, according to the “second” estimate released by the Bureau of Economic Analysis which appears to be positive news for employers and employees alike.

What are other buyers doing in terms of hiring? A recent ManpowerGroup Survey found 22% of US employers plan to increase staff in the second quarter, 4% plan to decrease staff, 72% expect no change in staff and 2% responded “didn’t know.” Employers in Nebraska, Idaho, Rhode Island and Iowa reported the strongest net employment outlooks, while Wyoming, Nevada, Louisiana and New Jersey project the weakest outlooks. It is worth noting that all four US regions surveyed by The ManpowerGroup reported a positive net employment outlook with employers in the Midwest and South regions reporting the strongest seasonally adjusted outlook at 17% each. The West region followed at 16% (a bit weaker than last year) while the Northeast reported a seasonally adjusted outlook of 15%.

Global buyers face an interesting global economic labor outlook. The predictions are fairly consistent and a recent Forbes article by economic consultant Bill Conerly gives some further detail. The article forecasts that commodity-dependent countries like Latin America, Africa and parts of Asia may be in for harder times but Asia itself may be a wild card given China’s reporting and Japan’s recession. Europe is looking at moderate growth and India remains strong due to consumer spending and low commodity prices.

Buyers may be looking at less need for temporary staffing in the manufacturing, warehousing and transportation sectors and possible lower demand in Latin America, Africa and parts of Asia. In terms of growth it look to continue in healthcare, professional services, construction and leisure/hospitality so be prepared to continue to be vigilant in looking for new sources to prepare and retain your suppliers and talent pools in these areas.