As I mentioned in my opening keynote to our European CWS Summit in April, a recent McKinsey survey suggests that the world saw (on average), a seven-year acceleration in the share of offerings that are of the digital nature between December 2019 and July 2020 (seven years in Europe, six years in North America and 10-plus years in Asia Pacific).

Within the staffing world, we can think of digital offerings as vendor management systems, extended workforce solutions, direct-sourcing platforms, the plethora of staffing platforms, interviewing aids, recruiterless solutions utilizing integrations of multiple systems and many others.

Development of technologies is only part of the story, however; their adoption is the true indicator of progress. What is the rate of adoption of MSPs’ service offerings and where do those rates fit overall?

Over the years, we have seen MSPs around the world enhance their product and service portfolios in response to the changing needs of their existing and potential customers. This has been happening at an ever-increasing rate over the last five to 10 years, especially with the enhanced capabilities afforded by technology and automation.

When thinking about rates of adoption, it is important to weight these according to the share of contingent workers around the world, as well as spend. For example, an adoption across a multinational program with thousands of workers and hundreds of millions of spend, needs to be weighted higher than an adoption of the same feature across a single location program utilizing just a few dozen workers and minimal spend.

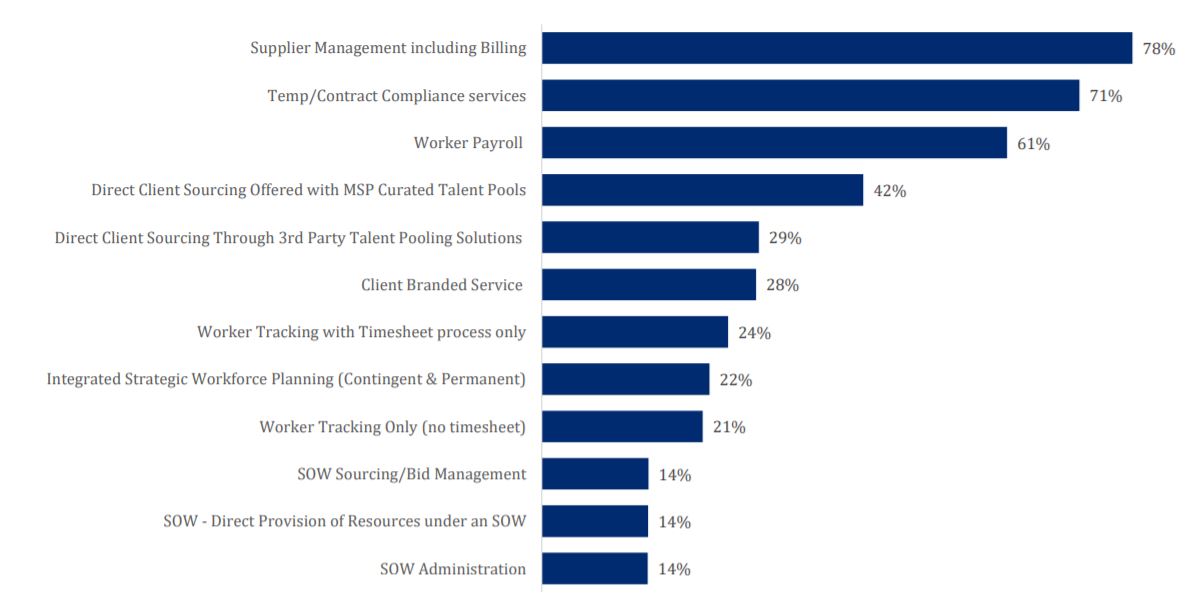

So, what are some of the most (and least) adopted MSP features according to our most recent ”MSP Global Landscape and Differentiators” report?

It is not surprising that “supplier management, including billing” accounts for the highest level of adoption — at 78% — given that this was the primary reason MSPs were set up in the first place.

With a growing trend around the world of driving both corporate and legislative compliance among the contingent workforce, it isn’t surprising that “temporary/contract compliance services” is second on the adoption list at 71%.

MSP Service Adoption. Source: MSP Global Landscape and Differentiators report.

What is quite surprising to me, however, is that fourth and fifth places are taken by “direct client sourcing offered with MSP curated talent pools,” at 42%, and “direct client sourcing through 3rd-party talent pooling solutions,” at 29%. While we are still early in the adoption cycle of “direct sourcing through 3rd-party talent pooling solutions,” the 29% adoption rate — remember, this is weighted according to volume of workers and spend within the overall program — is evidence to me of the growing interest and the likelihood that this channel will ultimately become predominant in our industry for many skill sets.

Meanwhile, what might surprise many is that the three lowest-ranked in terms of adoption — each at 14% — all relate to statement of work: “SOW sourcing/bid management,” “SOW-direct provision of resources under an SOW” and, finally, “SOW administration.”

The reason this might surprise buyers is that, according to our latest Workforce Solutions Buyer Survey, 54% of respondents said that SOW is already included within their overall contingent workforce program. When you compare this with the low adoption rates of SOW features within an MSP of 14%, this discrepancy indicates to me there is a common misunderstanding among buying organizations as to what is and, more importantly, what is not, statement of work. This is likely the reason why on the one hand buyers say SOW is included within the program, yet on the other hand, the MSPs are saying that the adoption of SOW services is very low.

I fully expect to see more alignment and understanding of the outsourcing of both projects and services under structured SOWs between buyers and providers in the next 12 months, and — along with the technology advancements we are seeing — a marked increase of the actual services procurement spend under management within structure contingent workforce programs over the next two years.

The MSP Global Landscape and Differentiators report is available to members of the CWS Council.